Understanding the complexities of financial transactions, especially with larger investments such as automobiles, often feels like an obstacle course for many.

This challenge is exacerbated by a myriad of terms and concepts that are thrown around, making the process seem more daunting.

This brings us to one pivotal concept in auto finance: car financing.

At first glance, it might seem like unfamiliar territory, but with the correct insights and perspective, it can be easily grasped.

Breaking down complicated financial jargon, we shall delve into the process, parameters, and peculiarities of this subject matter.

Our aim is to equip you with knowledge to navigate the ins and outs of car financing, allowing you to make informed decisions for your future automobile investments.

Contents

- What Does Financing A Car Mean?

- Understanding Car Financing: A Step-by-Step Guide

- The Factors That Influence Car Loan Eligibility

- The Role of Credit Score in Car Financing

- Exploring Different Types of Car Loans

- Secured Loans vs. Unsecured Loans: What’s The Difference?

- The Pros and Cons of Financing Directly Through a Dealership

- How Does Car Loan Interest Work?

- The Implications of Failing to Make Car Loan Payments

- Ways to Reduce Your Car Financing Costs

- Tips for Navigating Your First Car Financing Experience

- The Bottom Line

What Does Financing A Car Mean?

Financing a car means obtaining a loan to purchase the vehicle, typically from a bank, credit union, or directly from the dealership. The loan is then repaid over a specified period of time, with interest. This allows the buyer to use the car while making affordable payments, instead of needing the full purchase price upfront.

Expanding on this topic, it’s crucial to understand that car financing involves more than just the basic premise of acquiring a loan.

There are a variety of aspects that one must consider before opting for this financial tool, such as the implications of interest rates, down payments, financing terms, and credit score requirements.

Additionally, there are different types of auto finance agreements, each with its own unique characteristics and potential benefits or drawbacks.

In the following sections, we’ll delve deeper into these components to give you a comprehensive understanding of car financing and how it fits into your overall financial planning.

By the end of this article, you will be well equipped to make an informed auto financing decision that suits your specific financial situation and needs.

Understanding Car Financing: A Step-by-Step Guide

To navigate the potentially complex landscape of car financing, having proper understanding and meticulous guidance is vital. Car financing is simply a means by which you make payments towards owning a car, without having to shell out the full purchase price upfront. Instead, a financial lending institution such as a bank lends you the money, and you repay it over a specified period.

The exceptional benefit is the chance to own a vehicle that might be otherwise unattainable if you had to pay outright.

Though it sounds relatively straightforward, many facets require your attention to make an informed decision. These include determining your eligibility, understanding the role of your credit score, exploring loan types, grasping the workings of loan interest, and knowing the implications of non-payment.

Adoption of some practical car-financing cost reduction strategies and tips to help navigate your first car financing experience might come handy too.

Let’s delve into these steps in detail.

Determining Your Budget

As the first step, you need to determine the budget for your car purchase. Consider how much you can afford to pay monthly without straining your finances. Remember, the cost of owning a car goes beyond the purchase price — it includes auto insurance, maintenance, and regular gas usage.

Also, depositing a down payment upfront could lower your monthly repayments, so plan for it.

The basis of your affordability helps you narrow down the range of cars you can apply for financing on. It also advises you on the loan amount to request.

The establishment of a budget is paramount to an affordable car financing experience.

This budget exercise not only provides a clear financial picture but also prevents you from falling into severe debt. Remember, the aim of car financing is to make car ownership more attainable, not to lure you into unnecessary debt.

Choosing the Right Car

Once your budget is set, the next step is to choose the perfect car within your price range. It could be a brand-new vehicle, a used car, or even a leased car. The choice boils down to your preference, needs, and budgetary consideration.

Different makes, models, and the age of the car can affect financing options available to you, including interest rates and the length of loan terms.

Researching and comparing car models, their prices, and available financing options is a good strategy to find the best fit.

Always remember, a car is an investment that should serve you for a considerable period. Therefore, choose wisely.

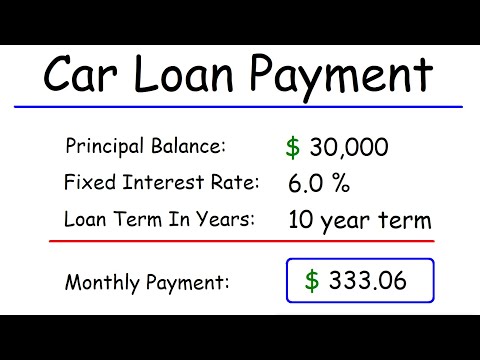

You can gain insights on how to calculate car loan payments from the embedded video above. It provides useful hacks on how to make the most of your investment.

Applying for a Car Loan

With your budget set and the right car chosen, it’s time to apply for the car loan. The lender provides the cash upfront to purchase the vehicle, and you repay the amount over the agreed loan term.

Upon application, the lender will consider several factors, including your credit score, income, employment stability, etc., to determine your eligibility.

If approved, you move on to sign loan documents, collect the funds, and purchase your dream car.

The car loan process involves checks and balances to ensure you’re able to repay the loan comfortably.

Remember, the main goal is to facilitate car ownership while promoting responsible borrowing. Therefore, lenders have to be thorough to minimize their risk of default.

Making Regular Payments

Once you have the car, the responsibility shifts to making regular loan payments. These monthly outflows should align with your initial budgeting efforts.

Ensuring regular payments protects your credit score, prevents late payment fees, and ultimately, leads to full car ownership. Be aware of all ramifications associated with non-payment; they can be severe.

In conclusion, managing your car financing can be plain sailing if you approach it wisely with an understanding of the relevant aspects involved. Remember to always borrow responsibly.

The Factors That Influence Car Loan Eligibility

When it comes to car financing, several crucial factors determine eligibility for the loan.

In the world of car loans, just like any other type of loans, lenders assess risk before granting someone financing.

Employment Status and Income

Foremost among the factors is employment status and income.

Most lenders want assurance that the borrower is capable of paying back the loan.

An individual must have a steady source of income that is sufficient enough to cover the regular car loan payments and other costs of living.

Typically, the borrower’s income needs to be verifiable, usually through pay stubs or tax returns.

Credit Score

Another critical factor that affects eligibility for a car loan is the borrower’s credit score.

A high credit score translates to less risk for the lender, which potentially leads to a more favorable interest rate for the borrower.

Lower credit scores often mean higher interest rates, assuming the lender grants the loan at all.

The higher the borrower’s credit score, the more attractive they become to lenders.

This simple fact suggests that maintaining a healthy credit score can be instrumental in securing a car loan with favorable terms.

Debt-to-Income Ratio

Moreover, lenders scrutinize a borrower’s debt-to-income (DTI) ratio.

This ratio compares the total monthly debts of an individual to their gross monthly income.

An acceptable DTI ratio demonstrates to lenders a borrower’s ability to manage monthly payment obligations against their earnings.

Generally, a DTI ratio of 43% or less is desirable to many lenders.

Loan Amount

The loan amount requested also impacts loan eligibility.

Lenders evaluate the loan-to-value ratio (LTV), which is a ratio of the loan’s amount to the value of the vehicle.

Typically, the lower the LTV, the more favorable terms the borrower may receive.

Lenders prefer an LTV of 80% or less as a way to lower their risk.

The loan amount and the resulting LTV ratio play a substantial role in determining car loan eligibility.

This indicates that a reasonable loan amount proportional to the value of the car can significantly enhance the chances of loan approval.

In summary, understanding the factors that influence car loan eligibility can help borrowers better prepare their loan applications and improve their chances of approval.

Although lenders may have slightly different criteria, these four factors – employment and income stability, credit score, debt-to-income ratio, and loan amount relative to the vehicle’s value – are omnipresent in their assessments.

The Role of Credit Score in Car Financing

Credit score is a numerical representation of your creditworthiness that lenders use to evaluate your eligibility for different forms of credit, including car loans.

The higher your credit score, the more likely lenders are to trust you with a loan because it indicates you have a history of paying back your debts on time.

Your credit score is determined by several factors, such as your payment history, the amount of debt you have, the length of your credit history, and the diversity of your credit.

Credit Score and Interest Rates

In the context of car financing, your credit score mainly affects the interest rate on your loan.

Lenders typically offer better interest rates to borrowers who have higher credit scores.

This is because such individuals represent a lower risk to the lender.

Therefore, a good credit score can massively affect the total cost of your vehicle purchase.

The Credit Score Car Dealerships Consider

When you apply for a vehicle loan through a dealership, they might look at a different credit score than the one you see on free credit score websites.

Dealerships often pull your auto-specific credit score, also known as your FICO Auto Score, which is a type of industry-specific credit score.

There are nine different FICO Auto Scores, and they’re specific to car lending.

You may gain insights into how dealerships use credit scores for car loan approvals from this highly recommended educational video.

It also sheds light on ways to improve your auto-specific credit score, which might boost your chances of securing a favorable car loan.

Improving Your Credit Score for Car Financing

The most significant stride you can make towards improving your credit score is making sure you pay all your bills on time, every time.

This not only includes your credit card bills, or any loans you might have but also your rent, utilities, phone bill and others.

A history of consistent and prompt payments demonstrates to lenders that you’re reliable and can be trusted with their money.

Your credit score is something you have control over and can improve with time and disciplined financial habits.

Improving your credit score is a journey, but the real challenge lies in maintaining it.

Ensure that you routinely check your credit score to prevent and quickly fix any errors which may negatively affect your rating.

Most importantly, live within your means and establish a stable history of credit use.

Wrapping Up

While your credit score plays a significant role in car financing, it should not discourage you from trying to secure a car loan.

Remember, a low credit score is not a dead-end, but an opportunity for you to build a healthier financial future.

Exploring Different Types of Car Loans

When it comes to car financing, borrowers have a variety of options to choose from.

These distinct categories of car loans come with varying interest rates, repayment terms, and conditions.

Conventional Auto Loans

Firstly, we’ll walk through the most common type, which is the Conventional Auto Loan.

This sort of finance is typically offered by banks, credit unions or online lenders.

Borrowers repay the loan with interest in fixed monthly instalments over a set period which typically ranges from three to seven years.

> Conventional Auto Loans offer a predictable repayment plan, which makes budgeting easier.The predictability of monthly repayments makes it easier to budget, and borrowers might have the potential to negotiate terms depending on their creditworthiness and the type of vehicle they intend to buy.

However, keep in mind that a larger down payment or a cosigner may be required, depending on the lender’s policies and the borrower’s credit history.

Dealer Financing

Next, there’s the option of Dealer Financing, a loan that’s provided through the car dealership from which you’re purchasing the vehicle.

With this type of lending, the dealership works as an intermediate between the borrower and the lender.

However, the convenience of one-stop shopping is often outweighed by higher interest rates and less attractive terms in comparison to conventional auto loans.

> It’s important to consider the potential downsides of Dealer Financing, such as higher interest rates and less attractive terms.While dealership financing might seem enticing due to the convenience of arranging finances and purchasing a car at one place, you should consider its potential downsides as well.

In some cases, the dealer might mark up the loan’s interest rate or include additional fees or hidden costs in the loan agreement.

Leases

Lastly, in addition to these traditional car loans, leases offer another form of vehicle financing.

With a lease, you’re not purchasing the car but renting it for a pre-agreed period.

While leases often require lower monthly payments, they do not contribute towards vehicle ownership.

> A lease can be an attractive option if you like driving newer cars and don’t mind that you’re not building equity in the vehicle.This form of financing can be attractive if you’re someone who prefers to drive newer cars and doesn’t mind not building equity in the vehicle.

However, there might be limitations on mileage and follow-up costs if you exceed those or terminate the lease early.

Secured Loans vs. Unsecured Loans: What’s The Difference?

When delving into car financing, understanding the difference between secured and unsecured loans is crucial.

These two types of loans represent entirely different financial agreements and could potentially have disparate impacts on your financial health.

Secured Loans Explained

A secured loan is a type of loan that requires you to provide collateral as a guarantee of repayment.

This collateral often comes in the form of the asset you’re financing— in this context, your car.

If you default on the loan, the lender has the right to take possession of your asset to recover the funds.

The potential loss of your vehicle is a significant risk of secured car loans.

However, due to the collateral, these loans typically come with lower interest rates.

Unsecured Loans Explained

On the other hand, an unsecured loan does not require any collateral.

These loans are granted based on your creditworthiness, which is determined through factors such as your income and credit score.

If you fail to make repayments, the lender cannot directly seize your assets.

The lender, however, may take legal action to recover the funds, which could adversely impact your credit score.

This more indirect risk signifies that unsecured loans typically have higher interest rates than secured loans.

They can also be tougher to obtain if your credit score isn’t in good standing.

Choosing Between Secured and Unsecured Loans

Choosing between a secured and an unsecured loan is largely a matter of personal preference and risk analysis.

If you’re comfortable using your car as collateral and are focused on lower interest rates, a secured loan might suit you best.

However, if risking your asset or property doesn’t sound appealing, and you have a good credit score, an unsecured loan could be a better option.

While this discussion provides insight into secured and unsecured car loans, this embedded video can help you understand how car loans affect your credit score.

Knowing this information can greatly influence your decision when choosing between a secured and unsecured loan.

The Pros and Cons of Financing Directly Through a Dealership

When buying a car, one of the most critical decisions that you need to consider is whether to finance directly through a dealership or to opt for another form of financing.

There are a few things you need to thoroughly consider when deciding on how to finance your car; this involves understanding the pros and cons of each option.

The Pros of Financing Directly Through a Dealership

One major advantage of financing directly through a dealership is convenience. When you finance directly through the dealership, you are essentially getting a one-stop-shop for all your car purchase needs.

Another advantage is that dealerships often have special promotions or incentives for those who choose to finance through them.

Dealerships also have the ability to negotiate loan terms on the spot, which can make the financing process more flexible and personalized.

Dealerships have the ability to negotiate loan terms on the spot, which can make the financing process more varied and personalized.

For buyers who may have a lower credit score, dealerships can sometimes be a more accommodating option as they might have relationships with a wider variety of lenders who are willing to take on riskier loans.

The Cons of Financing Directly Through a Dealership

Whilst a dealership can offer convenience and ease, there are also some potential downsides to financing directly through them.

For instance, the interest rates offered by dealerships can sometimes be higher than other financing options.

This is because they often mark up the interest rates from lenders as a way to compensate for their services.

Dealerships often mark up the interest rates from lenders as a way to compensate for their services.

This means that buyers could end up paying more in the long term. Another disadvantage is that dealerships might not always have your best interest in mind. Their ultimate goal is to sell, which can sometimes result in misinformation or pressure to agree to unfavorable terms.

Lastly, their array of options could be limited to what their partnered lenders offer, which means you may not be getting the best deal available in the market.

In summary, it’s essential to do your due diligence, asking questions and taking the time to compare and contrast options before deciding whether to finance directly through a dealership. Understanding both the pros and cons of this type of financing will enable you to make an informed decision that suits your personal financial situation.

How Does Car Loan Interest Work?

Understanding how car loan interest works is imperative if you’re planning to finance your next vehicle. The interest on car loans is an amount over and above the principle amount borrowed, which lenders charge for lending you the money.

Interest on car loans may be calculated either as simple interest or compound interest depending on the terms of the agreement. Simple interest is calculated using the principal amount, the interest rate, and the duration of the loan.

Car Loan Interest Calculation

Here’s how simple interest on a car loan is calculated: (Principal amount * Rate of interest * Time period) / 100.

However, many lenders also use compound interest for financing cars. In this case, the interest is calculated based on the outstanding balance of the loan after certain periods (monthly, half yearly, or annually).

Essentially, the longer you take to repay, the more interest you will pay, primarily because the interest is constantly calculated on the outstanding balance.

Therefore, if you make larger payments than required, you can prevent the outstanding amount from ballooning, thereby reducing the total interest paid.

Fixed vs. Variable Interest Rates

Car loans can have either a fixed interest rate or a variable interest rate. Fixed rates stay the same throughout the loan’s term, making the loan more predictable and the payment amounts and term fixed.

Conversely, variable rates can change over time according to the market fluctuation. These loans are riskier because if the rate of interest rises, so does your car payment.

While a fixed rate car loan is more predictable, a variable rate car loan may present an opportunity to benefit from declining interest rates.

Remember, taking on more risk can result in higher costs in the future if rates rise, so it’s crucial to consider your financial position and risk tolerance before opting for a variable rate car loan.

By watching the video embedded above, you may gain more insights into how different types of loans, including auto loans, affect your credit score. You’ll also learn more about the dynamics of rising and falling credit scores and various contributing factors.

Interest and Car Loan Duration

Finally, the duration of the loan also plays a major role in the overall interest paid. Long-term loans may have lower monthly payments, but over a longer period, the total interest paid may be significantly higher than that of a short-term loan.

Short-term loans might result in higher monthly payments with a lesser interest rate. Ultimately, it depends on your capacity to meet the monthly payments without affecting your financial health.

You should always choose a loan term that balances affordability of monthly payments with a reasonable total loan cost.

The Implications of Failing to Make Car Loan Payments

Your car loan repayment agreement is a legal contract and failure to make prompt payments can have serious implications. Let’s explore these in depth.

Damage to Credit Score

Missing a car loan payment can significantly impact your credit score.

Each missed payment is generally reported to credit bureaus, which is reflected on your credit report.

Such a dip in your credit score can affect you for several years, making it difficult to qualify for loans or credit cards in the future.

Bear in mind that late payments can remain on your credit report for up to seven years.

The longer you allow your debts to remain unpaid, the more your credit score will suffer.

Failing to make car loan payments can significantly reduce your credit score, affecting your borrowability in the coming years.

This could also result in higher interest rates on future loans, as lenders may perceive you to be a high risk borrower.

Even if you manage to secure a loan, you may end up paying hefty sums towards interest.

Repossession of the Vehicle

One of the most immediate and visible consequences of failing to make car loan payments is the risk of vehicle repossession.

Since most car loans are secured loans, the vehicle itself serves as collateral against the loan amount.

When you default on your loan payments, the lender has the right to reclaim or “repossess” your car. This can happen without any prior notice, depending on the laws in your state.

The repossession can take place anywhere—whether at home, at work, or in a public place.

When you default on a car loan, the lender has the right to repossess the vehicle without any notice.

Moreover, if the car sells for less than the outstanding loan amount, you could still be liable for the difference, further deepening your financial troubles.

Besides, having a repossession on your credit history can make it extremely difficult to get approved for future car loans.

Legal Consequences

Continual failure to pay your car loan or any attempt to avoid repossession can lead to serious legal consequences.

Firstly, you could be sued for the remaining unpaid debt, particularly in case of a significant outstanding balance.

Moreover, if you are sued and lose the case, the court could issue a judgment ordering you to pay the debt, which could lead to wage garnishment or a lien on your property.

Permanent damage to your credit report, as well as your ability to borrow in the future, are other potential legal consequences of failing to pay your car loan.

Ensure timely payments to avoid these consequences.

Legal consequences of not making car loan payments can include being sued for outstanding debt, wage garnishment, and property liens.

Therefore, it’s essential to understand the implications of not honoring your car loan agreement and take necessary steps to avoid such a situation.

In case you encounter difficulties making payments, it’s best to reach out to your lender as early as possible to discuss potential solutions.

Ways to Reduce Your Car Financing Costs

Car financing is an essential consideration for many who wish to own a vehicle. While it can present a convenient way to secure your dream car, it can also create a significant expense that lasts for several years. The good news is that there are ways to minimize your car financing costs and get the most value from your loan.

In this section, we’ll explore some practical ways to reduce car financing costs that you can use during your next purchase.

Improve Your Credit Score

The impact of your credit score on your car loan’s terms and interest rate cannot be overstated. Lenders use credit scores to determine your loan eligibility, the amount they’re willing to lend, and at what interest rate. Essentially, a higher credit score will open doors to lower interest rates and more favorable terms, ultimately reducing your financing costs.

Before applying for a car loan, look into your credit situation. Identify potential pitfalls, correct errors, and improve your credit standing if possible. There are various ways to achieve this, such as regularly paying your bills on time, minimizing your credit utilization rate, and avoiding unnecessary hard inquiries on your credit report.

Negotiate For A Better Deal

It’s often said that everything is negotiable, and this is also true for car loans. Many car shoppers focus on the price of the car without giving much thought to the financing costs. While negotiating the vehicle’s price is important, don’t neglect the possibility to negotiate the loan terms as well.

Interest rates, loan duration, and the terms of your contract can often be negotiated down, leading to cost savings in the long run. For example, if your credit has improved significantly since you took your loan, consider refinancing to achieve a better interest rate. Remember, every little bit of pragmatism and negotiation prowess can contribute to reducing your overall financing cost.

Negotiating the interest rates, loan duration, and contract terms can significantly reduce your financing cost.

This point cannot be emphasized enough. Reducing your interest rate, even by a small percentage, can result in substantial savings over the lifetime of your loan. Similarly, negotiating for a shorter loan duration can expedite your repayment timeframe, enabling you to own your vehicle sooner.

Opt For A Shorter Loan Term

Although longer loan terms mean smaller monthly payments, they come with higher interest costs in the long run. By opting for a shorter loan term, you can pay off the loan quicker and pay less in interest, significantly reducing your overall financing cost.

This option might require larger monthly payments, so be sure your budget can accommodate this adjustment before committing.

Watching the video will give you an insider look into the loan application process from a financial expert’s perspective. You will also discover additional strategies that can help you reduce your overall car financing cost.

In conclusion, reducing your car financing costs requires planning and informed decision-making. It’s essential to consider all these factors and strategies to ensure you make a financially sound decision on your car loan.

Embarking on your first car financing journey can seem daunting.

However, with proper preparation, understanding, and smart decision-making, you can navigate this process successfully.

1. Research and Pre-Approval Process

It is essential to start by researching about car financing even before you step into the dealership.

Get to know the terms, concepts, and how everything works to ensure that you’re getting a good deal.

Moreover, getting pre-approved for a loan from your bank or credit union before car shopping gives you leverage in negotiation and a better understanding of what you can afford.

“And, shopping for lenders gives you an advantage to compare the terms and pick the best deal for you.”It’s also a great way to know how much car you can afford and helps to narrow down your car choices before you even step onto the lot.

These steps will give you confidence and control over your car financing experience.

2. Credit Score

Recognize the role your credit score plays in determining your loan eligibility and interest rates.

Lenders use it to evaluate your creditworthiness and risk level.

A higher credit score generally positions you to secure a loan at favorable interest rates, while a lower credit score will make your financing more expensive.

“Maintaining a good credit score is crucial in obtaining a favorable car loan.”Make sure you know your credit score before you start shopping for a loan and work on improving it if needed.

Understanding where you stand credit-wise can be incredibly beneficial when discussing your financing options.

3. Understanding Loan Terms

Getting familiar with car loan terms is another valuable step in the car financing process.

You should understand the principal, interest, APR, loan term, and monthly payments, among others.

For example, a longer loan term means lower monthly payments but will end up costing you more in interest over the life of the loan.

“A sound understanding of the loan terms helps make an informed decision about your car financing.”Don’t be afraid to ask questions if you are unsure about any term. Clarifying doubts at the outset can save you from unpleasant surprises down the line.

It will also ensure that you are fully aware of what you sign up for.

4. Read the Fine Print

When reviewing the loan agreement, make sure to read the fine print.

There may be clauses about early payment penalties, default penalties, or add-ons that you didn’t ask for.

Thoroughly understanding the complete terms and conditions could save you from future financial troubles.

“Thoroughly reading and understanding the loan agreement can protect you from hidden costs and unpleasant surprises.”Remember, if you don’t understand something, it’s better to ask for clarification rather than to remain unsure.

Armed with these tips, first-time car financing shouldn’t be as scary as it may initially appear.

The Bottom Line

Navigating the world of car financing can indeed seem complex but with a well-grounded understanding of the process, it becomes significantly more manageable.

Key factors such as your credit score and loan eligibility play crucial roles, as do the different types of loans available, secured and unsecured.

Additionally, it’s important to understand all the terms involved, including dealership financing and how loan interests work.

Failing to make car loan payments can have serious implications, but there are effective ways to reduce your financial cost.

Ultimately, for a smooth first car financing experience, knowing what to watch out for and how to manage the process is key.

As with many aspects of personal finance, informed decision-making and careful planning are your most valuable tools.