Navigating the world of auto financing can be a daunting task.

Yet, understanding the intricacies of car loans is crucial when planning a vehicle purchase.

This knowledge can empower you to make the best decisions about your finances.

Whether you’re a first-time buyer or a seasoned car owner, it’s essential to comprehend the terms and conditions associated with this type of loan.

By familiarizing yourself with the process and the mechanisms behind it, you are setting the stage for affordable repayments and a sustainable financial future.

We’ve put together comprehensive guidance to help demystify the complexities of car loans.

Contents

- How Do Car Loans Work?

- Understanding Car Loans: A Step-by-Step Guide

- Understanding the Types of Car Loans

- The Importance of Credit Score in Car Loans

- How Much Can You Afford? Determining Your Budget

- Understanding Interest Rates and Car Loans

- Loan Terms and Conditions: What to Look For

- How Does Car Loan Pre-Approval Work?

- The Pros and Cons of Dealer Financing

- Tips for Securing the Best Car Loan Deal

- What Happens When You Default on a Car Loan?

- The Bottom Line

How Do Car Loans Work?

Car loans are a type of personal loan where the borrowed money is used specifically to purchase a vehicle, typically from an auto dealership. The borrower repays the lender, usually a bank or credit union, in monthly installments over a predetermined period of time. The vehicle itself often serves as collateral for the loan, meaning if the borrower defaults on payments, the lender can repossess the car.

Delving deeper into the topic, various key aspects of car loans warrant further examination to provide a comprehensive understanding.

Financial factors such as interest rates, credit scores, loan terms, and down payments significantly influence the overall cost of the loan and must be thoughtfully considered when securing a car loan.

It’s also critical to explore the different types of car loans available, along with their specific pros and cons, to identify the ideal financing solution tailored to your individual needs.

Also to be analyzed are the potential repercussions of defaulting on a car loan and potential strategies to mitigate such risks.

Stay tuned as we dive further into these intricate topics surrounding car loans.

Understanding Car Loans: A Step-by-Step Guide

Acquiring a car loan can be a daunting process, particularly for first-time buyers. The complexity surrounding the terms and conditions, interest rates, and other components often confuse many potential car owners. Therefore, it is crucial to understand the steps involved in processing a car loan for a seamless and stress-free experience.

Initiating the Car Loan Process

The first step in obtaining a car loan involves defining your car preferences and budget. Understanding your financial capabilities and the type of car you desire are key in determining the subsequent steps of the process. Besides, determining your car choice and budget narrows down your search, saving time and effort.

Once you have a clear idea of the car value and your budget, it is time to research the various lenders and their specific loan terms. This information is crucial in identifying a lender that aligns with your financial situation and needs.

Application and Approval

Upon identifying a suitable lender, the next step involves the completion and submission of the loan application form. Providing accurate and adequate information increases the chances of loan approval. The lender then reviews your application, verifying the details provided, such as employment history, income, and credit score, before making a decision.

In a scenario where you are pre-approved for a car loan, the lender often specifies the loan amount, the interest rate, and the term of the loan. This pre-approval allows you to have a predefined budget while shopping for a car, enhancing the efficiency of the search process.

Finalizing the Car Loan

A successful loan approval leads to the finalization step. This phase involves the drafting of loan terms and conditions and signing of the loan agreement. Here, it’s essential to fully understand the loan agreement before signing to prevent future disappointments or disputes.

Once the agreement is signed, the loan amount is disbursed to the dealer’s account or directly to you, depending on the agreed terms. This marks the commencement of your loan repayment period according to the agreed schedule.

> “A successful loan approval leads to the finalization step.”This sentence emphasizes the importance of loan approval in progressing to the final stages of the car loan process. After successful approval, the borrower and lender can proceed to finalize the loan agreement, marking the commencement of the repayment period.

This video elaborates on the specifics of car loan interest rates. It can broaden your perspective on how different factors affect these interest rates and subsequently impact your loan repayment. This information would be invaluable for both first-time car buyers and those looking to secure better loan terms in their subsequent purchases.

Understanding the Types of Car Loans

To effectively explore the various types of car loans, it is important to start by understanding the definition of a car loan. This is a specific type of personal loan that a person takes to purchase a vehicle.

The Different Categories of Car Loans

Car loans can be classified into various categories. The two broad categories of car loans are new car loans and used car loans. As the names suggest, new car loans are for the purchasing of new cars while used car loans are taken to finance the purchase of preowned or second-hand cars.

The difference between these two loans is primarily seen in the interest rate attached to each. New car loans typically attract lower interest rates than used car loans.

Another crucial difference between these two types of car loans is the loan value. New car loans typically provide a higher loan amount than used car loans.

These differences are important because they directly influence the overall cost of buying a car. Thus, it pays to understand the dynamics at play in both cases before making a decision.

The difference between new and used car loans is primarily seen in the interest rate attached to each and the loan value.

This quote highlights that the choice between a new car and a used car loan should not merely be driven by the condition of the car but also by the financial implications.

The interest rate and loan value differences account for the notion that used cars are cheaper to buy but more expensive to finance while new cars are expensive to buy but cheaper to finance.

Secured and Unsecured Car Loans

Another way to classify car loans is into secured and unsecured loans. A secured car loan is one where the car that you purchase is used as collateral for the loan. If you default on the loan, the lender can repossess the car to recover their money.

On the other hand, an unsecured car loan is one where no collateral is required. In the event of a default, the lender has no specific property to seize. However, they can take other collection actions such as engaging collection agencies or suing you.

The key difference between the two is the risk level. Since secured loans pose less risk to the lender, they typically come with lower interest rates. Unsecured loans, being riskier, often carry higher interest rates.

The key difference between secured and unsecured loans is the risk level.

The statement explains why people with a stable income and good credit history often go for secured loans for the lower rates, while those with a shaky credit history might prefer unsecured loans to avoid the risk of repossession.

However, both options have their benefits and downsides, and understanding this can help borrowers to make informed choices.

In conclusion, understanding the types of car loans and their characteristics is essential. It helps potential borrowers make informed financial decisions that suit their economic status and car ownership goals.

The Importance of Credit Score in Car Loans

Understanding the role of a credit score in securing car loans is a fundamental step in the process of acquiring a vehicle through financing.

What is a Credit Score?

A credit score is a number generated by a mathematical algorithm that evaluates your creditworthiness.

It considers multiple factors including your payment history, the amount of debt you have, and the length of your credit history.

Your credit score acts as a snapshot of your financial credibility at a certain point in time.

Lenders use this information to assess the risk of extending credit to you.

A higher score signifies less risk, making you an attractive borrower.

Why is a Credit Score Important for a Car Loan?

In the context of car loans, your credit score plays a crucial role in determining whether you will be approved for a loan.

The better your credit score, the higher your chances of securing a car loan.

Besides approval, your credit score also affects the interest rates offered to you.

Generally, those with higher scores are privy to more favorable interest rates, leading to lower overall costs.

This is because lenders consider borrowers with high scores less likely to default on their loan repayments.

Besides approval, your credit score also affects the interest rates offered to you.

This quote reinforces the idea that a better credit score can greatly improve the terms and conditions of your car loan.

Essentially, a good credit score can potentially save you a significant amount of money over the duration of your car loan.

This is why it’s crucial to understand your credit score before beginning the car loan application process.

Watching this video can help you understand more about how car loan payments work.

It provides valuable insight into how to use your credit score effectively when applying for a car loan.

Improving Your Credit Score

If your credit score is not as high as you’d like, don’t despair.

There are several proactive steps you can take to improve your score before applying for a car loan.

Paying bills on time, reducing outstanding debts, and keeping credit balances low are some ways to boost your credit score.

Remember, a higher credit score can unlock better car loan options and help you save a significant amount of money.

Addressing credit problems head-on demonstrates to lenders that you are responsible and provides them with more confidence in your ability to repay your loan.

How Much Can You Afford? Determining Your Budget

Affordability: A Vital Consideration

Determining your budget for a car loan is the initial step you must take before exploring any further options.

The amount you can afford to pay every month will significantly impact the type of car you can purchase, how long the loan will last and the interest rates you are offered.

It is essential to consider your monthly income and expenses when figuring out how much you can set aside for a car loan.

Understanding the limit of your affordability is a pivotal step in a car purchase.

Having a clear picture of your financial capacity not only prevents you from falling into debt but also ensures that you choose a car within a realistic price range.

Therefore, making a comprehensive budget plan at the start of the process helps you to keep track of your finances and stay within your means.

Devising a Comprehensive Budget Plan

The first step in drafting a budget involves assessing your current financial status.

Your main and auxiliary sources of income, mandatory expenditures like rent or mortgage, bills, food, insurance among others should all be taken into account.

It is also important to consider any potential future expenses, or economic circumstances that might affect your ability to repay the car loan.

Future planning is a critical aspect of devising a comprehensive budget plan.

Potential future expenses or hardships could put strain on your financial health causing you to default on your car loan. Therefore, an effective budget plan should take into account potential future expenditures as well.

After understanding your financial standing, calculate how much you can afford to pay every month for your car loan. This amount should be something you can comfortably shell out every month without stretching your finances.

Another aspect to take into account when determining your budget is the down payment.

Usually, the higher the down payment, the lower your loan amount will be. This means lower interest costs over the loan tenure.

Besides the down payment, there are also car-related expenses like maintenance, insurance, and fuel costs that you need to incorporate into your budget.

Down payment and car-related expenses can significantly affect your total car budget.

Paying a larger down payment can help you save in the long run as it could lead to a lower interest rate and decrease the size of your monthly payments. However, it’s important to ensure the down payment amount doesn’t strain your current finances.

With car-related expenses, keep in mind that these are recurring prices and need to be factored into your monthly expenses. These additional costs should not lead to a financial strain.

Monitoring Your Budget

Finally, once you have established a budget plan for your car loan, it’s important to continually monitor this plan and update it as necessary.

The ongoing maintenance of your budget is just as crucial as its initial creation, as this allows you to stay within your spending limits while ensuring that changes in your financial situation are accounted for.

Maintaining your budget is pivotal to successful car loan repayment.

By constantly gauging your budget, you can ensure that you are not sinking into financial troubles. Additionally, it allows you to plan for any necessary adjustments based on fluctuations in your income or expenses.

In conclusion, determining your budget for a car loan is a crucial process that needs careful consideration and ongoing scrutiny. It sets the tone for your car loan journey and helps to ensure that your financial health remains intact.

Understanding Interest Rates and Car Loans

When diving into the world of cars loans, interest rates play a vital role.

The interest rate is a percentage of the loan that’s charged as a fee over a specific period.

This can dramatically influence the overall cost of your vehicle.

How Interest Rates Work

Firstly, it’s important to understand that the interest rate on a car loan is essentially the cost of borrowing money.

For every dollar you borrow, you’ll need to pay back that dollar plus an additional small percentage of that dollar.

The interest rate is represented as a percentage of the loan amount, usually calculated on an annual basis, known as the annual percentage rate (APR).

By watching this video, you will ensure you understand the difference between the interest rate and APR. You’ll also be more aware of what you should be looking for when analyzing loan offers.

Factors Affecting Interest Rates

Various factors can influence the interest rate you’re offered on your car loan.

One crucial element is your credit score; generally, higher credit scores merit lower interest rates due to perceived reduced risk.

Loan term length also impacts the rate, interestingly shorter-term loans often have lower interest rates but higher monthly payments.

The vehicle’s age and whether it’s new or used can also contribute to the interest rate decision.

The vehicle’s age and whether it’s new or used can contribute to the interest rate decision.

This is because lenders often consider used cars to be higher risk, leading to higher interest rates. It’s important to remember however that rates can vary widely between lenders, so it’s always wise to comparison shop.

Understanding these factors that affect interest rates can guide your choices and help you save money on your car loan.

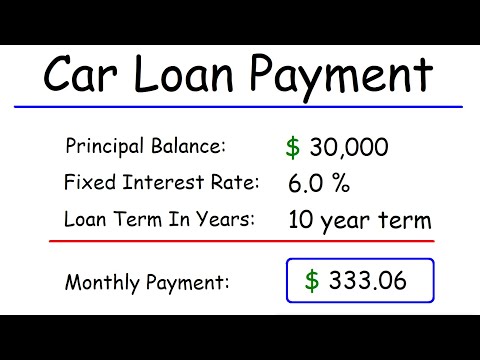

How to Calculate Interest on Car Loans

Understanding how to calculate interest on your loan will allow you to estimate future payments and plan your budget responsibly.

In most cases, car loans use simple interest, which adds the interest onto the principal loan amount.

The formula to calculate simple interest is I = PRT, where ‘I’ is the Interest, ‘P’ the principal amount, ‘R’ the rate of interest per period, and ‘T’ the time the money is borrowed for.

Starting with this baseline understanding of interest rates on car loans can help make sense of your loan and budget appropriately.

Loan Terms and Conditions: What to Look For

Choosing a car loan can be an overwhelming process, especially when it comes to understanding the terms and conditions that come along with it.

Interest Rate and Annual Percentage Rate (APR)

One of the first things to look out for in a car loan contract is the interest rate.

This is the amount of money you’ll be charged for borrowing, expressed as a percentage of the total loan amount.

More importantly, though, you should focus on the Annual Percentage Rate (APR).

This figure includes not only the interest rate, but also other charges and fees associated with the loan, providing a more accurate picture of the true cost of the loan.

Therefore, when comparing different loan offers, APR can be a more useful comparison tool than the basic interest rate.

The Annual Percentage Rate (APR) of a car loan includes not only the interest rate, but also any other charges and fees, providing a more accurate understanding of the true cost of the loan.

It’s crucial to understand that a loan with a slightly higher interest rate but a lower APR might actually be a cheaper option.

That’s because it will cost less over the entire term of the loan due to lower fees and charges.

Loan Term Length

The next major consideration is the length of the loan term.

A loan term is the period of time over which you will be repaying the borrowed amount.

Typically, car loan terms range from two to seven years.

While a longer term means lower monthly payments, it also means you’ll pay more in interest over the life of the loan.

A loan term is the period of time over which you will be repaying the borrowed amount, and while a longer term means lower monthly payments, it also means more interest over the life of the loan.

Therefore, it’s often better to go for the shortest loan term that you can afford in order to minimize the total interest paid.

Fees and Penalties

Another crucial aspect to watch out for in a car loan contract are any additional fees and penalties.

For example, some loans feature early repayment penalties, which charge you a fee if you pay off your loan ahead of schedule.

Others might have origination fees or loan setup fees which could increase the total cost of your loan.

Additionally, some loans might have penalties for missed or late payments, so it’s important to be aware of these potential costs.

Early repayment penalties, origination fees or setup fees could increase the total cost of your loan, while penalties for missed or late payments could further compound your debt.

Be sure to avoid loans with excessive fees and penalties, even if they offer attractive interest rates or loan terms.

The key is to read the loan agreement thoroughly before signing to ensure you’re not caught off guard by hidden costs.

How Does Car Loan Pre-Approval Work?

When it comes to purchasing a car, a crucial step in the process is getting car loan pre-approval. The pre-approval process helps you determine how much you can afford and gives you a clearer budget when car shopping.

Getting pre-approved for a car loan means that a lender has agreed, in principle, to lend you a specific amount to buy a car. This is based on factors such as your income, credit score, and other financial commitments.

With a pre-approved loan, you can negotiate as a cash buyer, which can give you an advantage in the negotiations process. It also simplifies the buying process as it reduces uncertainty about your budget.

Getting pre-approved for a car loan means that a lender has agreed, in principle, to lend you a specific amount to buy a car.

This quote highlights that pre-approval essentially puts you in a position where you’ve got the money ready to pay for a car, up to the pre-approved amount. It’s like walking into a dealership with cash-in-hand, which can give you an advantageous position when negotiating.

However, pre-approval doesn’t guarantee that you’ll get the loan. The lender will still need to check the vehicle details and could still turn you down for various reasons. For example, if the car is overpriced, or if it’s too old or has too many kilometres on it.

Finding the Right Lender for Pre-Approval

When seeking pre-approval, it’s essential to shop around. Different lenders may offer different interest rates and terms, so you should compare several lenders to find the best deal.

Every lender will have their own eligibility criteria, so find one that suits your individual circumstances. Some lenders may specialize in loans for people with bad credit, while others might offer better rates to those with an excellent credit score.

It’s essential to be aware that each time you apply for a loan, it can affect your credit score. Applying for several loans over a short period can lower your score and make it harder for you to get approved.

Every lender will have their own eligibility criteria, so find one that suits your individual circumstances.

This statement emphasizes the importance of finding the right lender based on your unique situation. Not every lender will be a good fit for you, so it’s important to do your homework and compare different offers.

Once you’ve found a few potential lenders, you can then start the pre-approval process. This usually involves completing an application form and providing details about your income, expenses, and any other outstanding debts.

For more in-depth insights on securing a car loan, this video can be a handy guide. It discusses the key factors that influence car loan approval, giving you a comprehensive take-away to navigate this process with ease and confidence.

In conclusion, understanding how car loan pre-approval works can give you a competitive advantage and help you negotiate better terms. A solid understanding of car loans can help you make informed decisions and secure the best possible deal.

The Pros and Cons of Dealer Financing

Dealer financing is a popular option that allows the car dealership to act as both the seller and lender. Many car buyers feel this is a convenient one-stop-shop for their vehicle purchasing needs. However, like any financial decision, dealer financing has its own set of advantages and disadvantages.

Pros of Dealer Financing

Dealer financing offers a level of convenience that is hard to beat. Instead of needing to secure financing independently from another financial institution, car buyers can do everything in one place.

Special financing offers are often available from the dealership. These may include low or zero percent interest rates, cash back offers, and other attractive promotional deals that you might not find elsewhere.

The dealership typically handles all the paperwork, which can take some of the stress and hassle out of the financing process.

Furthermore, dealer-financed contracts are flexible. You can often negotiate the terms, such as the length of the contract and the amount of the down payment.

Overall, the key benefits of dealer financing are its convenience, promotional offers, ease of paperwork, and flexibility.

This can make the car buying process smoother and possibly more cost-effective, particularly if you can snag a special financing offer. Dealerships have relationships with multiple lenders, which allows them to seek out the best loan terms for your situation.

Cons of Dealer Financing

Despite the benefits, there are also downsides to dealer financing that are important to consider.

One downside is that the dealership might not have your best interest in mind when determining your loan terms. Their primary goal is to sell cars, and they may propose financing options that are more beneficial to them than to you.

Moreover, dealer financing could lead to higher overall costs. For instance, dealer-based financing might come with higher interest rates than what you’d find with credit unions or banks.

There could also be hidden costs in a dealer financing arrangement. These might include various additional fees or costs wrapped into your loan that could catch you by surprise later on.

It’s more difficult to compare loan offers when dealing with dealer financing. You may miss out on better loan terms elsewhere because it’s hard to shop around when the dealership is doing all the dealing.

All things considered, the primary drawbacks of dealer financing include potentially being subject to higher interest rates, hidden fees, and difficulty comparing offers.

Therefore, before opting for dealer financing, it’s worth shopping around to ensure you’re getting the best deal. Even if you decide to go with dealer financing, having a quote from another lender can give you leverage in negotiations.

Conclusion

Ultimately, the choice between dealer financing and other loan options depends on your specific circumstances and preferences. Both the pros and cons should be considered deeply before making a decision.

In the end, it’s crucial that car buyers are aware of all their financing options, understand the terms of their loan contract, and make the best financial decision for their individual situation.

Tips for Securing the Best Car Loan Deal

Securing the best car loan deal requires thorough research, understanding key loan principles, and savvy negotiation. A car is a significant investment and leveraging the right loan can significantly impact your financial health.

Know Your Credit Score

Before delving into the car loan process, it’s paramount that you understand your credit score. Lenders use this score to determine your loan eligibility and the interest rate they offer. A higher score generally results in a lower rate, translating to considerable savings over the life of the loan.

A sound understanding of your credit score will put you in a strong negotiating position.

There are various platforms where you can check your credit score for free, ensuring you are fully informed before approaching lenders.

Understanding your credit score can save you thousands on your car loan.

This is because lenders perceive individuals with higher credit scores as less risky, thus granting them lower interest rates. Endeavour to continually improve your credit score by maintaining healthy financial habits such as meeting deadlines for bill payments and reducing outstanding debt.

Comparison Shopping

Simply accepting the first loan offer you get is a common mistake among many car buyers. Instead, you should shop around and compare different lenders’ offers. This practice, known as comparison shopping, will help you find the best car loan deal with competitive interest rates and favourable terms.

It’s advisable to explore both traditional banks and credit unions as they may offer different advantages. Also, consider online lenders as they often have competitive rates.

Comparison shopping aids in sourcing the most favorable car loan deal.

By comparatively analyzing diverse loan offers, you’ll have a comprehensive understanding of the prevailing market rates and terms, enabling you to make an informed decision. Always factor in the loan term, the monthly payments, and any potential hidden fees when comparing loan offers.

Understanding car loan interest is integral to securing a favorable car loan deal. The aforementioned video succinctly explains this concept in an easily digestible manner. By gaining this knowledge, you’ll be equipped to better negotiate your car loan terms.

Negotiating Your Car Loan

Negotiation is a significant aspect of securing the best car loan deal. The price of the car, the interest rate, and the terms of the loan are all negotiable. It’s crucial not to focus solely on the monthly payment but to consider the total cost of the loan.

Coming into these negotiations with a pre-approved loan can also provide you with a strong bargaining chip. It puts you in a position of power and can encourage the dealer to offer better terms to secure the sale.

Effective negotiation is crucial in securing a favorable car loan.

It’s important to remember that the final monthly payment is not the only factor to consider. You need to ensure that the loan term, the interest rate, and the total cost of the loan are all within your comfort zone. Negotiating these aspects can help you secure a loan deal that fits well within your budget and financial plan.

What Happens When You Default on a Car Loan?

Understanding Defaulting on a Loan

Defaulting on a car loan reflects a failure to uphold the agreed terms of the loan, usually involving a failure to make the designated payments on time.

This event represents a serious breach of contract and can have significant repercussions for the individual involved.

The specific parameters defining default can vary, but it generally occurs after a borrower has missed multiple payments.

Typically, lenders will start the process of repossession in such instances, because in their perception, this would minimize their losses.

Defaulting on a car loan represents a serious breach of contract and can initiate the repossession process.

The implications of this are far-reaching and it’s essential to understand that the lender tends to see default as a last resort since the repossession process is costly and time-consuming.

In many cases, the lender would prefer to work out a payment plan with the borrower, rather than opting for repossession.

Consequences of Loan Default

The ramifications of defaulting on a car loan are manifold and some of them can be quite severe.

As we’ve already mentioned, repossession of the vehicle is one of the most dramatic outcomes.

It is important to keep in mind that even if your car is repossessed, you are not absolved of the obligation to pay the outstanding balance on your loan.

Additionally, defaulting will have a negative impact on your credit score, making it more difficult to secure lending in the future.

Even if your vehicle is repossessed, you still need to repay the remaining balance on your loan.

Default can also lead to higher interest rates when you try to secure new credit, and in severe cases could lead to wage garnishment where a portion of your income is appropriated to pay off the debt.

The fact that default results in a severe blow to creditworthiness underscores the importance of considering all potential consequences when contemplating a car loan.

Preventing Loan Default

If you find yourself struggling to make your car loan payments, take immediate action.

Reaching out to your lender to discuss your financial situation could lead to an alternative payment plan that prevents default.

Remember, as earlier stated, lenders typically prefer to avoid default situations wherever possible – a practical stance that could work in your favour.

You might also consider options like refinancing the loan, or selling the vehicle to pay off the debt.

Early communication with your lender might help establish a tailored payment plan, offering a lifeline in the face of potential loan default.

Takeaway: Defaulting on a car loan has serious implications.

Understanding these impacts, as well as options for preventing default, can help you make more informed decisions about your financial situation.

The Bottom Line

Navigating the landscape of car loans can be tricky, but understanding the different types, the importance of credit scores, and how much you can realistically afford helps pave the way.

Knowing the ins and outs of interest rates, loan terms, pre-approvals, dealer financing, and refinancing can empower you to secure a beneficial deal.

While exercising caution in maintaining your creditworthiness and always making payments on time can protect you from the repercussions of defaulting.

Keep all these useful insights in mind to enlighten your decision-making process when taking on a car loan.

The right knowledge equips you to negotiate the most advantageous terms, ultimately serving your best financial interests, and ensuring that your car financing journey is as smooth and worry-free as possible.