Understanding the mechanics of car loans is essential for any prospective buyer looking to finance their new vehicle.

With an abundance of options out there, navigating this landscape can seem quite daunting.

The process involves a series of steps, all of which are crucial in ensuring that you get the most beneficial deal.

This includes learning about interest rates, loan terms, and payment calculations.

By diving deep into these complex concepts, we aim to clarify and simplify them.

Thus, ensuring that you’re well-equipped with all the necessary knowledge before stepping into a car dealership.

Contents

- How Do Car Loan Work?

- Understanding the Basics of Car Loans

- How Are Interest Rates Determined for Car Loans?

- What Are the Steps Involved in Securing a Car Loan?

- Decoding the Car Loan Terminologies

- The Significance of Credit Score in Car Loan Application

- Understanding the Loan Repayment Process

- The Role and Risk of Collateral in Car Loans

- Fixed Vs. Variable Interest Rates: Which One to Choose?

- Consequences of Defaulting on Your Car Loan

- Options for Refinancing Your Car Loan

- The Bottom Line

How Do Car Loan Work?

A car loan operates as a purchase agreement where a lender provides the borrower with the funds to purchase a vehicle, and the borrower agrees to repay the total loan amount, plus interest, over a fixed period of time. The lender will hold the car’s title as collateral until the loan is fully paid off. If the borrower fails to make the agreed payments, the lender has the right to repossess the vehicle.

Expanding upon this, it’s crucial to consider the additional elements that factor into the dynamics of a car loan.

We will delve into a detailed analysis of aspects such as the impact of credit scores on loan eligibility, the decision between new and used cars, loan pre-approval, and various loan terms and conditions.

Further discussion will clarify these intricate aspects and equip readers with a deeper understanding of how car loans function in different scenarios.

The goal is to provide a comprehensive resource for both prospective borrowers and those simply interested in financial concepts.

So, let’s proceed to unwrap the layers of the car loan process.

Understanding the Basics of Car Loans

Car loans, also known as auto loans, are fundamentally a type of loan that a consumer secures to purchase an automobile.

Generally provided by a financial institution like a bank or credit union, car loans allow you to borrow a lump-sum from the lender and repay the amount overtime plus interest.

Car loans can be a crucial tool for potential car owners as it eases the financial burden of making a large, upfront payment.

When acquiring a car loan, there are several key elements to consider which may include: principal amount, interest rates, loan term, and monthly payments.

The Principal Amount and Interest Rates

The principal amount refers to the initial amount borrowed that is used to purchase the vehicle while the interest rates, determined based on various factors, is the cost charged for borrowing that money.

Your loan term is the agreed upon period within which the loan must be fully repaid.

Interest is accumulated over time and is usually expressed as a percentage of the principal amount.

One must also note that your monthly payments are not just paying off the principal amount, but also the accumulated interest.

The interest rate on your loan can greatly affect the total cost of the car once it’s been completely paid off.

Thus, understanding how interest rates work and how they are calculated is essential in making a prudent financial decision when securing a car loan.

Consequently, it is always wise to shop around for the most favourable interest rates and terms before settling on a lender.

Tackling Car Loan Terminologies

When navigating the world of car loans, it’s crucial to understand some commonly used jargon in the industry.

Terminologies like down payment, APR (Annual Percentage Rate), loan-to-value ratio (LTV), or depreciation can be confusing for a first time auto loan borrower.

For clarity on how these terms impact your car loan and to make the most out of your borrowing experience, it’s crucial to educate yourself about these terminologies.

Just like this YouTube Video:

https://www.youtube.com/watch?v=POzbXK87Cag.

This particular video provides a detailed and straightforward explanation of interest rates on car loans.By watching it, you will acquire a better understanding of how interest rates are determined, which will significantly help in your decision-making process.

The Importanace of Your Credit Score

The last but crucial element to consider when applying for a car loan is your credit score.

Typically, a higher credit score will potentially make you eligible for a more favourable interest rate as it indicates credit worthiness to the lender.

Your credit history can directly impact the final interest rate offered on your car loan.

So, it’s essential you are aware of your credit score and history to avoid any surprises during the application process.

Equally important, it’s always a good idea to take steps in boosting your credit score before applying for any major loans such as a car loan.

How Are Interest Rates Determined for Car Loans?

Understanding the factors that influence the interest rates of car loans is a crucial step towards securing a favorable deal.

Credit Score

Credit score plays a key role in determining car loan interest rates.

Lenders use it to assess the risk involved in lending money to an individual.

Those with high credit scores are considered as low-risk borrowers and are offered a lower rate of interest.

On the other hand, if you have a poor credit score, lenders see you as a high-risk borrower and charge a high interest rate to offset the potential risk.

This makes it incredibly important to maintain a good credit score if favourable interest rates are to be attained.

High credit scores are associated with low-interest rates, as individuals with these scores are viewed as low-risk borrowers.

A good credit score strongly indicates that an individual has a good track record when it comes to repaying their debts on time.

It puts lenders at ease knowing that their money will likely be returned within the agreed-upon timeframe.

Loan Duration

The length of the loan term also greatly influences the interest rate.

Short-term loans usually come with lower interest rates.

This is because the lender’s money is at risk for a shorter period, and therefore, the lender charges less interest.

On the other hand, long-term car loans typically have higher interest rates due to the increased risk associated with the extended timeframe.

The length of the loan term directly impacts the interest rate. Short-term loans typically have lower rates, while long-term loans see higher rates.

It’s important to bear in mind that while long-term loans might seem attractive due to small monthly payments, the overall interest paid over the loan’s lifespan tends to be higher.

Opting for a shorter loan term can result in substantial savings in the long run.”

Economic Factors

Lastly, broader economic factors such as inflation, the state of the economy, and central banks’ policies can influence car loan interest rates.

When the economy is performing well, interest rates tend to rise due to increased borrowing and spending.

In contrast, during an economic downturn, interest rates usually fall to encourage borrowing and stimulate economic activity.

Consequently, timings of the economy can be a determining factor of car loan interest rate.

Economic conditions significantly affect car loan interest rates. High rates are seen during booming economic activities, whereas low rates are likely during an economic downturn.

Staying informed about the global and national economic trends can help borrowers monitor changes in car loan interest rates and apply at the optimum time.

This helps in securing the most favorable loan conditions.

What Are the Steps Involved in Securing a Car Loan?

Securing a car loan involves a few crucial steps that are not only pivotal to grasp an understanding of but also the difference between securing a good loan and a poor one.

It is vital to recognize that obtaining a car loan is not an overnight task but a process that requires planning, budgeting, an understanding of your credit score, comparing loan offers, and ultimately, the closing of the loan.

Step one starts with gathering enough information about the new car you want to purchase or the used car you’re interested in.

If buying a new car, it’s essential to assess the market price and the manufacturer’s suggested retail price (MSRP).

Understand Your Credit Score

Next, you need to carefully evaluate your credit score which is a vital part of the car loan process.

It is necessary to understand that a higher credit score may translate to better car loan interest rates because lenders view you as a less risky borrower.

Your credit score directly impacts your car loan’s interest rate and, consequently, the amount you’ll pay back over time.It’s important to enter the auto loan process knowing your credit score or at least have an idea of it.

This will help you have a better sense of the loan terms and conditions you are likely to receive, even before you apply for the actual loan.

Choose a Suitable Car Loan

The next step involves choosing a lender and evaluating various car loan options.

Different lenders may offer varying interest rates, terms, and fees.

It’s crucial to understand that while getting pre-approved for a car loan isn’t always necessary, it gives you a better idea of what you may be qualified to receive and can help you set a budget for your car purchase.

Car loan pre-approvals can also enable negotiations on better car prices with dealers.Therefore, it is advisable to explore all possible lenders including online lenders, banks, credit unions, and other loan services prior to settling for the best offer that matches your specific needs.

Once you have been pre-approved and have chosen a lender, you can now move forward and negotiate and finalize the terms of your car loan, ensuring you’re capable of making the monthly repayments.

Finalizing and Closing the Loan

The final process involves closing the loan, which means agreeing to the loan terms and signing the loan documents to secure the car loan.

Keep in mind that it is important to read and understand all the paperwork before signing any loan documents.

Ensuring that you understand every aspect of the car loan documents can save you from future disappointments caused by skipped over details.

It’s important to fill out all the paperwork correctly and adhere to all the steps we’ve outlined to avoid any hiccups in your car loan buying process.

Besides the steps discussed, securing a car loan process might involve other steps depending on personal circumstances and requirements.

This video discusses the details and nuances of car loan interests. It would provide further clarification about how your car loan interest might affect the total loan amount.

Watching the video also provides you with a practical perspective on how interest rates work with car loans, and would help you better navigate the car loan terrain.

Decoding the Car Loan Terminologies

The world of car loans encompasses many complex terminologies. Here, we will strive to decode and simplify some of the most commonly encountered terms to provide you with a clearer understanding.

Principal

The principal refers to the original amount of money you borrow for the car loan. This amount doesn’t include any interest or additional fees.

This term is one of the most basic components of a car loan, which further underscores its importance.

Understanding the principal sum is an essential first step in managing your car loan efficiently.

Once you grasp this concept, it becomes easier to work out how much you owe and plan your repayments accordingly.

Interest

Interest is the cost you pay for borrowing the principal sum. It’s usually expressed as a percentage of the borrowed amount and is calculated on an annual basis – commonly referred to as the interest rate.

This term is another crucial component to understanding how your monthly car loan repayments are determined.

Understanding the interest rate and its impact on your repayment sum is crucial in making informed financial decisions.

By factoring in the interest when considering a car loan, you can better assess whether the loan is affordable and suitable.

Amortization

The term amortization refers to the gradual reduction of the loan amount over the repayment period. A part of each repayment goes toward the principal, while the rest goes toward the interest.

By using an amortization schedule, you can understand how much of your monthly payment is going toward the principal and how much is going toward the interest at any given time.

“Amortization schedules offer valuable insight into how your car loan repayments are divided between the principal and the interest.“

This in-depth understanding enables you to get a clear perspective on how long it will take to pay off your loan and how much it will finally cost you.

Equity

Equity in context of car loans, refers to the car’s value that you truly own. It is the difference between the car’s current market value and what you still owe on it.

If you have positive equity, it means your car is worth more than what you owe, but if you have negative equity (also known as being “upside-down”), your car is worth less than what you owe.

Equity plays a significant role in deciding your financial standing in terms of your car loan.

Having a clear comprehension of these terms not only helps navigate the world of car loans more smoothly, but also empowers you to make better-informed financial decisions regarding your car purchase.

The Significance of Credit Score in Car Loan Application

Your credit score essentially paints a picture of your financial responsibility and creditworthiness. Hence, it plays a pivotal role in the car loan application process.

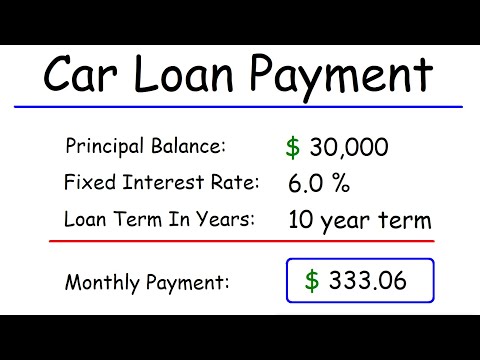

This video will provide you with a detailed explanation on how to calculate your car loan payments. It could significantly help in managing your finance better during the repayment process.

How Your Credit Score Affects Interest Rates

One primary reason your credit score is significant is its direct influence on the interest rates you get for your car loan. The better your score, the lower interest rate you can expect.

Lenders usually reserve their most competitive rates for borrowers with exceptional credit.

This means that maintaining a high credit score can save you substantial money in the long run.

One primary reason your credit score is significant is its direct influence on the interest rates you get for your car loan.

This is because lenders assess the risk associated with lending money based on credit scores. A higher score signifies lesser risk and vice versa.

Thus, you’re rewarded with lower interest rates if you maintain good financial habits.

The Relationship Between Credit Score and Loan Approval

Besides interest rates, your credit score could also directly impact your loan approval chances.

Most lenders have a credit score threshold below which they generally do not approve loans. This is because a lower score signifies higher lending risk.

Meeting the minimum required credit score is usually essential for loan approval.

Most lenders have a credit score threshold below which they generally do not approve loans.

Therefore, before applying for a car loan, you should make sure your credit score meets the lender’s threshold.

This can significantly improve your chances of loan approval and prevent unnecessary hits to your credit score caused by the loan application.

Improving Your Credit Score

If your credit score isn’t up to the mark, there are several ways to improve it.

Regular and timely payments of your bills, reducing your debt, and periodically checking your credit reports for errors are key to maintaining/improving your credit score.

With effort and consistency, you can elevate your credit score over time and enhance your chances of qualifying for favorable loan terms.

With effort and consistency, you can elevate your credit score over time and enhance your chances of qualifying for favorable loan terms.

Remember, improving your credit score is not an overnight process. It needs patience and a consistent effort in maintaining good financial habits.

With a higher credit score, not only does the chance of loan approval increases, but you might also enjoy lower rates and more favorable terms.

Understanding the Loan Repayment Process

When talking about car loans, the loan repayment process is a fundamental aspect to consider.

The loan repayment process starts with a plan, which breaks down how much you need to pay monthly over a specified period.

Loan Repayment Schedule

A repayment schedule outlines the timeline for repaying the loan.

It is usually set up in a way that the borrower makes equal monthly payments.

The payments are distributed to cover both the principal amount and the accrued interest.

However, the exact distribution between the principal and interest payments may vary over time, depending on the loan’s terms.

> The monthly payments consist of both principal and interest, but the distribution may vary over time, depending on the loan’s terms.Understanding this distribution can be crucial as it allows you to know exactly where your money goes every month.

For example, for loans with an amortizing schedule, initial payments cover more interest than the principal, but as time progresses, this ratio shifts in the principal’s favor.

Loan Term

The loan term significantly impacts the payment structure of the loan.

A longer loan term translates to lower monthly payments, but more interest accrued over time.

Thus, while it may seem beneficial in the short term due to lower monthly payments, a longer loan term essentially makes the loan more expensive in the long run.

> A longer loan term translates to lower monthly payments, but more interest accrued over time, making the loan more expensive in the long run.Conversely, shorter loan terms have higher monthly payments but for less time, reducing the total interest paid throughout the term.

Borrowers must therefore align the loan term with their current and projected financial situation to avoid strains in payments.

Prepayment and Late Payment Penalties

Some car loans come with the option for prepayments whereby you can clear your loan earlier than scheduled.

However, not all loans have favorable prepayment terms. Some impose prepayment penalties that could make the early payoff less beneficial.

It’s therefore important to understand the terms of prepayments for your specific loan.

> Prepayment penalties could make the early payoff less beneficial, hence it’s important to understand the terms of prepayments for your specific loan before deciding to prepay.Aside from prepayment, understanding the potential consequences of late payments is also crucial in the loan repayment process.

Most loans impose penalties for late payments, which can increase the overall cost of the loan.

Making Timely Loan Payments

Lastly, but most importantly, making timely payments is critical to avoid late fees and the potential risk of defaulting on your car loan.

Consistent timely payments will also improve your credit score, which could prove beneficial for future financial transactions.

Some tools, such as auto-pay or payment reminders, can be helpful to ensure you never miss a payment deadline.

> Making timely payments not only keeps you on track with your loan but also improves your credit score.The importance of this consistency can not be overstated, as it directly impacts both your current loan repayment and future financial engagements.

While the loan repayment process may seem challenging, understanding these key aspects can help you navigate it more effectively and optimize your finances.

The Role and Risk of Collateral in Car Loans

When discussing car loans, it is critical to understand the concept of collateral. It plays a pivotal role in the lending process.

A car is often used as the guarantee or collateral in a car loan, ensuring the borrower adheres to the loan agreement’s conditions.

Role of Collateral in Car Loans

Collateral is a lender’s safety net. In the case of car loans, the vehicle itself usually functions as the collateral.

This means, if a borrower falls behind on their car loan payments, the lender has the legal right to repossess the car.

This gives the lender some assurance of getting a portion of their money back, even if the borrower defaults on the loan.

After watching the embedded video, you will get more insights into how simple interest loans work, which is the basis for most car loans. Understanding this will further help you gauge the role of collateral in car loans.

It is noteworthy to understand that the use of a car as collateral is risky for the borrower but provides a safety mechanism for the lender.

This is because if the borrower is unable to keep up with their payment schedule, they run the risk of losing their car.

However, from the lender’s perspective, the use of collateral considerably reduces their risk as they have something tangible to retrieve their funds from in the event of a default from the borrower.

Risks Associated With Collateral in Car Loans

The primary risk associated with using your car as collateral in a car loan is the potential for repossession.

If you are unable to make your payments on time and default on your loan, the lender may take back, or repossess, the vehicle.

Repossession can have severe ramifications, including a significant impact on your credit score, which could make it harder to obtain credit or loans in the future.

This is why it is essential to understand the contract terms fully before committing to any loan, especially secured ones such as car loans.

Aligning your budget with the loan’s monthly payments and terms can help minimize the risk of default and subsequent repossession.

Sound financial management and gradual repayment of the loan are the key to avoid the risk of car repossession.

Understanding your financial situation, planning for the loan repayments, and maintaining a regular payment schedule can help mitigate the risks associated with collateral in car loans.

It’s also beneficial to look for the best loan terms that suit your financial capabilities.

Make sure to do extensive research before making a commitment to lessen the possible financial strain in the future.

Fixed Vs. Variable Interest Rates: Which One to Choose?

When choosing a car loan, one of the key decisions to make is whether to opt for a fixed or variable interest rate.

Both types have their own benefits and drawbacks, and the ideal choice largely depends on your personal circumstances and financial capacity.

Understanding Fixed Interest Rates

With fixed interest rates, the interest rate remains unchanged throughout the term of the loan.

This means your repayment amount will remain constant, regardless of any fluctuations in the market interest rates.

One of the major advantages of fixed interest rates is that they offer financial stability and predictability.

You will know exactly how much you have to pay each month, and this can make it easier to budget and plan your finances.

On the downside, if market rates fall, you will end up paying more interest than necessary since your rate will stay the same.

Fixed interest rates offer financial predictability as your repayment amount remains constant throughout the life of your car loan.

Choosing a car loan with a fixed interest rate may be a wise decision if you prefer to stay on the safe side and avoid the risk of potentially higher payments in unpredictable market conditions.

It would also be a logical choice if current market interest rates are low, and you anticipate a rise in the near future.

Understanding Variable Interest Rates

In contrast, variable interest rates fluctuate over time depending on the changes in the market interest rates.

This means your loan repayments could vary from one month to another, making budgeting somewhat challenging.

The advantage, however, is that if market rates decrease, so would your interest payments, potentially saving you money in the long run.

On the flip side, if market rates increase, your interest payments would go up, leading to a higher overall loan cost.

Variable rates may be an attractive option if you’re willing to bet on interest rates’ future behavior and if you’re comfortable with the risk of payment fluctuations.

Variable rates offer potential savings if market rates decrease, yet they pose a risk of increased payments if rates rise.

For those with a steady income and a certain level of risk tolerance, choosing a car loan with a variable interest rate could be a cost effective option, given they’re prepared for possible increases in loan payments.

It could also be a good choice when the market rates are expected to fall in the near future.

Making an Informed Decision

In conclusion, the decision between fixed and variable interest rates is essentially a matter of personal preference and risk tolerance.

Both have their pros and cons, and understanding these can help you make an informed decision based on your unique circumstances and financial goals.

Whether you choose fixed or variable rates, the key is to ensure the repayments are affordable and fit seamlessly into your budget while meeting your desired goals.

Making an informed decision about interest rate types requires a clear understanding of your financial capacity, risk tolerance and future interest rates anticipation.

Consulting with a financial advisor or a loan expert can provide more personalized advice tailored to your situation, helping you to choose the best car loan for your needs and future financial growth.

Consequences of Defaulting on Your Car Loan

When you enter into a car loan agreement, you are making a commitment to repay the borrowed amount plus interest over a specific period of time.

What happens though if you fail to uphold this agreement and default on your car loan?

Falling Into Default

The process of default typically begins after you have missed one or more loan payments.

Your lender will likely contact you, reminding you of your missed payment(s) and urging you to make a payment as soon as possible.

If you continue to ignore these notices, your lender can declare you to be in default.

It’s important to understand that defaulting on a car loan is a serious legal matter.

Effects of Default

A loan default can have many negative consequences.

Most immediately, your car may be repossessed by the lender as a means to recover the debt.

Your credit score will also take a significant hit, which can have long-lasting effects.

Additionally, you might incur extra costs from late payment fees or repossession expenses.

Once you default on your loan, your lender could demand that you pay the entire remaining balance at once.

This sudden demand for full payment can lead to serious financial distress.

If you cannot pay off the debt quickly, your other assets could be at risk.

Glimmer of Hope

Despite the many negatives associated with a car loan default, there are a few ways to avoid or curb the damage.

For instance, you can try negotiating with your lender to create a payment plan that is manageable within your financial constraints.

Refinancing your car loan is also an option, especially if your credit score has improved since taking out the original loan.

Ultimately, it’s in your best interest to do everything you can to avoid defaulting on your car loan.

Watching this video may provide additional information about understanding the basics of loans, including the importance of making regular loan repayments and the potential consequences of falling into default.

It also offers useful tips on how to avoid defaulting on your loan.

Options for Refinancing Your Car Loan

Refinancing your car loan can be a beneficial financial move, especially if your financial circumstances have changed since you first took out the loan.

Essentially, refinancing involves replacing your current loan with a new one which usually has more favorable terms.

There are a few key reasons you might consider refinancing your car loan such as lower interest rates, reduced monthly payments, to consolidate debt, or if your credit score has improved.

However, it’s crucial to carefully consider the right time to refinance and the impact that it can have on your financial health.

When to Refinance Your Car Loan

The best time to refinance your car loan is often when interest rates have dropped or when your credit score has significantly improved since taking the loan.

Another good time would be when you are finding it difficult to meet up with monthly payments. Refinancing can help reduce your monthly repayments and ease financial stress.

However, it’s important to evaluate whether the cost of refinancing will outweigh the benefits. Remember that applying for a new loan can have a small, temporary impact on your credit score.

> Refinancing can help reduce your monthly repayments and ease financial stress.It is also crucial to note that you should be careful about extending the loan term significantly. While this can lower monthly payments, it also means you pay more over the lifetime of the loan.

Types of Car Loan Refinancing

The first and most common type of car loan refinancing is traditional refinancing. This involves taking out a new loan, often with a different lender, with a lower interest rate or a longer term than your original loan. This generally leads to lower monthly payments, reducing your overall financial burden.

Next, there’s cash-out refinancing which involves taking out a loan for more than you owe on your car. The difference is then paid out to you in cash. This option is most beneficial when you have built up considerable equity in your car.

However, cash-out refinancing can be risky as you could end up owing more than your car is worth—that’s known as being “upside down” or “underwater” on the loan.

> Taking out a loan for more than you owe on your car is known as cash-out refinancing.Nonetheless, if used wisely, cash-out refinancing can provide you with an opportunity to consolidate high-interest debt, or cover necessary expenses.

How to Refinance Your Car Loan

To refinance your car loan, the first step is to shop around and compare lenders. Not every lender will provide refinancing and rates can greatly vary so it pays to do your homework.

Your credit score plays a significant role in the terms of your new loan. A higher credit score generally leads to more favorable terms.

Once you’ve found a lender with favorable terms, you’ll need to apply for the new loan. If approved, the new lender will pay off your existing loan, and you’ll start making payments to the new lender.

However, before you proceed with refinancing, you should be sure to fully understand the terms and conditions of the new loan.

Some loans might have penalties for early repayment or carry other hidden fees. Always read the fine print before signing.

> Always read the fine print before signing the refinancing agreement.Refinancing can truly benefit you—if done correctly. Therefore, it’s essential to understand all the possible scenarios that come with it.

The Bottom Line

Car loans can be a vital tool in making vehicle ownership affordable and attainable.

However, it essential to understand the basics, including how interest rates are determined and the steps involved in securing a loan.

Familiarity with car loan terminologies, significance of credit score, loan repayment process, and role and risk of collateral is beneficial.

A clear understanding of the differences between fixed and variable rates enables better decision-making.

Be aware of the consequences of defaulting and options for refinancing.

Remember, knowledge is your greatest ally, and understanding the fundamentals, through to complex aspects and frequently asked questions, can aid you in making wise, informed decisions regarding car loans.